What is Working Capital and How to Calculate: Your Complete Guide to Financial Success

Working capital represents one of the most fundamental concepts in corporate finance, serving as a critical indicator of an organization’s short-term financial health and operational efficiency. Defined as the difference between current assets and current liabilities, working capital provides insights into a company’s ability to meet its immediate obligations while maintaining smooth operational processes.

This financial metric extends beyond mere numerical calculation to encompass strategic decision-making processes that directly influence organizational liquidity, profitability, and long-term sustainability.

The significance of working capital management cannot be overstated in contemporary business environments, where cash flow optimization and resource allocation efficiency determine competitive advantage. Organizations across various industries must navigate the delicate balance between maintaining adequate liquidity for operational needs and minimizing excess capital that could otherwise be deployed for growth initiatives.

This comprehensive analysis examines the theoretical foundations, practical applications, and strategic implications of working capital management, providing a detailed exploration of how effective capital utilization contributes to organizational success and financial performance optimization.

Theoretical Framework of Working Capital

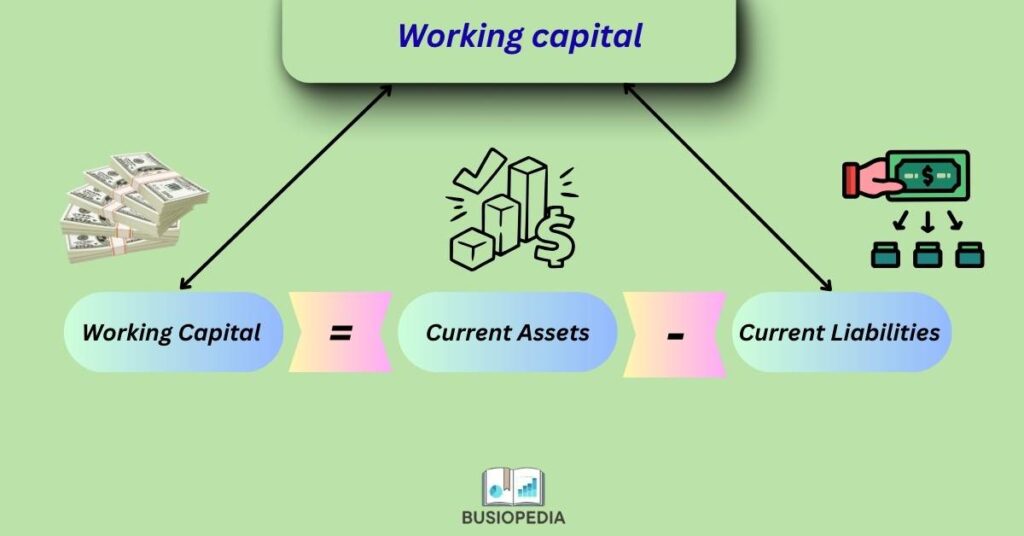

The mathematical formulation of working capital, expressed as Current Assets minus Current Liabilities, represents a deceptively simple equation that encompasses complex financial relationships and operational dynamics. The fundamental calculation is:

Working Capital = Current Assets – Current Liabilities

Where:

- Current Assets = Cash + Marketable Securities + Accounts Receivable + Inventory + Prepaid Expenses

- Current Liabilities = Accounts Payable + Short-term Debt + Accrued Expenses + Taxes Payable

Example Calculation: Consider ABC Manufacturing Company with the following financial position:

Current Assets:

- Cash: $500,000

- Accounts Receivable: $1,200,000

- Inventory: $800,000

- Prepaid Expenses: $100,000

- Total Current Assets: $2,600,000

Current Liabilities:

- Accounts Payable: $600,000

- Short-term Debt: $400,000

- Accrued Expenses: $200,000

- Total Current Liabilities: $1,200,000

Working Capital = $2,600,000 – $1,200,000 = $1,400,000

This positive working capital of $1,400,000 indicates the company has sufficient liquid assets to cover short-term obligations with a substantial safety margin.

Key Financial Ratios and Calculations

Current Ratio = Current Assets ÷ Current Liabilities

Using ABC Manufacturing: $2,600,000 ÷ $1,200,000 = 2.17. This indicates the company has $2.17 in current assets for every $1.00 of current liabilities.

Working Capital Turnover = Annual Sales ÷ Average Working Capital

If ABC Manufacturing has annual sales of $8,400,000, Working Capital Turnover = $8,400,000 ÷ $1,400,000 = 6.0 times. This means the company generates $6.00 in sales for every $1.00 of working capital.

Days Sales Outstanding (DSO) = (Accounts Receivable ÷ Daily Sales) × 365

Daily Sales = $8,400,000 ÷ 365 = $23,014 DSO = ($1,200,000 ÷ $23,014) × 365 = 52.2 days Customers take approximately 52 days to pay their invoices.

Days Inventory Outstanding (DIO) = (Inventory ÷ Daily COGS) × 365

If the Cost of Goods Sold is $5,040,000 annually: Daily COGS = $5,040,000 ÷ 365 = $13,808 DIO = ($800,000 ÷ $13,808) × 365 = 58.0 days. Inventory is held for approximately 58 days before sale.

Days Payable Outstanding (DPO) = (Accounts Payable ÷ Daily COGS) × 365

DPO = ($600,000 ÷ $13,808) × 365 = 43.5 days. The company takes approximately 44 days to pay suppliers.

Cash Conversion Cycle = DSO + DIO – DPO

CCC = 52.2 + 58.0 – 43.5 = 66.7 days. The company’s cash is tied up in operations for approximately 67 days.

Academic literature has established several theoretical perspectives on optimal working capital management. The traditional approach emphasizes maintaining sufficient liquidity to meet operational obligations, prioritizing financial stability over profit maximization.

Conversely, the modern approach advocates for minimizing working capital investment while ensuring operational continuity, thereby maximizing return on assets and enhancing shareholder value. Contemporary research suggests that optimal working capital levels vary significantly across industries, organizational size, and market conditions, necessitating tailored management strategies rather than universally applicable solutions.

The pecking order theory provides additional theoretical context, suggesting that internal financing through working capital optimization represents a preferred funding source compared to external debt or equity financing. This perspective emphasizes the strategic importance of efficient working capital management in reducing dependency on external financing sources and maintaining operational autonomy.

Types and Classifications of Working Capital

Working capital classifications provide frameworks for understanding different aspects of liquidity management and operational financing requirements. Gross working capital refers to the total value of current assets without considering current liabilities, providing insight into the absolute magnitude of short-term resources available to an organization.

Net working capital, calculated as current assets minus current liabilities, represents the more commonly utilized measure that indicates the excess of liquid assets over immediate obligations.

Positive Working Capital

Positive working capital occurs when current assets exceed current liabilities, generally indicating favorable liquidity conditions and the ability to meet short-term obligations. For instance, a manufacturing company maintaining $2 million in current assets against $1.5 million in current liabilities demonstrates positive working capital of $500,000, suggesting adequate liquidity for operational needs.

Negative Working Capital

Negative working capital, characterized by current liabilities exceeding current assets, may appear concerning, but it can represent efficient capital utilization in certain business models. Retail giants like Walmart often operate with negative working capital by collecting cash from customers before paying suppliers, effectively using supplier financing to fund operations.

The distinction between permanent and temporary working capital reflects the varying nature of liquidity requirements across business cycles.

Permanent Working Capital

Permanent working capital represents the minimum level of current assets necessary to maintain basic operational capacity, remaining relatively stable regardless of seasonal or cyclical fluctuations. For example, a pharmaceutical company requires consistent minimum inventory levels for essential medications regardless of market conditions.

Temporary Working Capital

Temporary working capital fluctuates with seasonal demands, promotional activities, or economic cycles. Agricultural businesses exemplify this classification, requiring substantial temporary working capital during planting and harvesting seasons while maintaining minimal permanent working capital during dormant periods.

Components Analysis with Industry Examples

Accounts receivable management represents a critical component of working capital optimization, directly influencing cash flow timing and credit risk exposure. Retail organizations like Target implement sophisticated credit management systems that balance customer accessibility with collection efficiency.

Through automated credit scoring, dynamic payment terms, and proactive collection procedures, retail companies optimize the trade-off between sales volume and cash conversion speed. Advanced analytics enable these organizations to identify high-risk accounts early, implement appropriate collection strategies, and minimize bad debt expenses while maintaining customer relationships.

Inventory management constitutes another fundamental aspect of working capital optimization, particularly relevant for manufacturing organizations. Toyota’s implementation of just-in-time inventory systems exemplifies efficient inventory management that minimizes carrying costs while ensuring production continuity.

By coordinating closely with suppliers and implementing demand forecasting systems, Toyota maintains minimal inventory levels without compromising manufacturing schedules. This approach reduces storage costs, minimizes obsolescence risk, and frees capital for alternative investments while maintaining operational efficiency.

Accounts payable optimization demonstrates how strategic payment management can enhance working capital efficiency. Technology companies like Apple leverage their substantial market power to negotiate extended payment terms with suppliers while maintaining strong vendor relationships.

By extending payment periods from 30 to 60 days, Apple effectively utilizes supplier financing to fund operations and invest in research and development initiatives. This strategy requires careful balance to avoid damaging supplier relationships while maximizing cash flow benefits.

Cash management practices vary significantly across service industries, where inventory requirements are minimal, but accounts receivable management remains crucial.

Consulting firms like McKinsey & Company implement rigorous cash management protocols that include detailed project billing procedures, milestone-based payment collection, and sophisticated cash flow forecasting systems. These practices ensure adequate liquidity for operational expenses while minimizing idle cash balances that could be deployed more productively.

Working Capital Management Strategies

Conservative working capital management prioritizes liquidity and financial stability over profit maximization, maintaining higher current asset levels relative to current liabilities. This approach provides substantial safety margins for meeting unexpected obligations or capitalizing on strategic opportunities. Pharmaceutical companies often adopt conservative strategies due to regulatory requirements and long product development cycles.

Pfizer, for instance, maintains substantial cash reserves and inventory buffers to ensure regulatory compliance and product availability while absorbing potential market disruptions or research and development setbacks.

Aggressive working capital management emphasizes profit maximization through minimal working capital investment, accepting higher liquidity risks in exchange for enhanced returns on assets. Technology startups frequently employ aggressive strategies to maximize growth potential while conserving scarce capital resources.

Companies like Uber initially operated with minimal working capital by leveraging driver and customer payments to fund operations while minimizing traditional inventory and receivables investments. This strategy enabled rapid expansion but required careful risk management to avoid liquidity crises.

Moderate working capital management seeks to balance liquidity requirements with profitability objectives, maintaining adequate safety margins while avoiding excessive capital deployment. Manufacturing companies like General Electric implement moderate strategies that consider cyclical demand patterns, supplier relationships, and customer payment behaviors.

This balanced approach provides operational flexibility while optimizing returns on invested capital through careful monitoring of working capital components and adjustments based on market conditions.

Risk-return trade-offs inherent in working capital decisions require sophisticated analysis of potential outcomes and their respective probabilities. Higher working capital levels generally reduce financial risk but may indicate inefficient capital utilization. Lower working capital levels enhance profitability metrics but increase vulnerability to operational disruptions or market volatility. Effective management requires continuous evaluation of these trade-offs and adjustment of strategies based on changing business conditions and strategic objectives.

Industry Case Studies and Comparative Analysis

Manufacturing sector working capital management exemplifies the complexity of balancing production requirements with financial efficiency. Boeing’s working capital management involves coordinating extensive supplier networks, managing long production cycles, and accommodating customer advance payments.

The company maintains substantial work-in-process inventory due to aircraft production timelines while utilizing customer deposits to partially finance operations. Boeing’s working capital turnover ratio of approximately 6.5 times annually demonstrates efficient capital utilization despite complex operational requirements.

Retail sector examples highlight the importance of inventory management and seasonal fluctuations in working capital requirements. Home Depot’s working capital strategy involves sophisticated inventory forecasting systems that anticipate seasonal demand patterns, regional variations, and promotional requirements.

During peak spring seasons, the company increases inventory levels and extends supplier payment terms to manage cash flow effectively. Home Depot’s negative working capital of approximately -$2.8 billion demonstrates efficient use of supplier financing while maintaining customer service levels.

Service sector organizations face unique working capital challenges related to accounts receivable management and minimal inventory requirements. Professional services firms like Deloitte focus primarily on optimizing collection procedures and project billing cycles. These organizations typically maintain positive working capital due to prepaid expenses and accounts receivable, but minimal inventory requirements simplify overall working capital management. Service companies generally achieve higher working capital turnover ratios due to reduced inventory investments.

Cross-industry comparison reveals significant variations in optimal working capital levels and management strategies. Manufacturing companies typically require higher working capital levels due to inventory and production requirements, while service companies operate with minimal working capital needs. Technology companies often demonstrate negative working capital through efficient cash collection and extended supplier payment terms. Retail companies may operate with either positive or negative working capital depending on their specific business models and market positioning.

Impact on Financial Performance and Valuation

The relationship between working capital management and profitability demonstrates complex interactions that extend beyond simple correlation analysis. Efficient working capital management enhances profitability through reduced financing costs, improved asset utilization, and enhanced operational flexibility.

Companies that optimize working capital components typically achieve higher return on assets ratios and improved profit margins through reduced carrying costs and more efficient resource allocation. Cash flow effects of working capital management directly influence organizational liquidity and financial stability.

Improvements in working capital efficiency generate immediate cash flow benefits through reduced asset investment requirements or extended liability payment periods. These cash flow enhancements provide resources for strategic investments, debt reduction, or dividend payments, contributing to overall financial performance and stakeholder satisfaction.

Valuation implications of working capital management affect investor perceptions and market valuations of publicly traded companies. Efficient working capital management signals effective operational management and financial discipline, potentially supporting higher valuation multiples. Investors frequently analyze working capital trends and efficiency metrics when evaluating investment opportunities, recognizing the strategic importance of liquidity management in long-term organizational success.

Academic research consistently demonstrates positive correlations between effective working capital management and various performance metrics, including profitability, growth rates, and market valuations. Studies across multiple industries and geographic regions confirm that organizations with superior working capital management practices generally outperform peers in financial performance measures and market recognition.

Key Takeaways

Critical Success Factors

- Develop a comprehensive understanding of industry-specific working capital requirements

- Implement appropriate technological systems for real-time monitoring and analysis

- Establish continuous monitoring of key performance indicators and metrics

- Create tailored strategies aligned with unique operational characteristics and market conditions

- Avoid generic approaches that may prove ineffective for specific business contexts

Best Practices for Implementation

- Coordinate all working capital components in integrated management systems

- Monitor accounts receivable, inventory, accounts payable, and cash simultaneously

- Consider interdependent relationships between different working capital elements

- Focus on cumulative effects on overall financial performance rather than isolated optimization

- Implement comprehensive systems that provide holistic visibility across all components

Strategic Management Priorities

- Emphasize continuous improvement in working capital efficiency through regular assessment

- Conduct benchmarking against industry standards and competitor performance

- Implement technological solutions that enhance automation and decision-making capabilities

- Ensure leadership commitment to working capital optimization initiatives

- Allocate appropriate resources and organizational focus to critical financial management activities

Long-term Implications

- Recognize that working capital management extends beyond short-term liquidity considerations

- Build foundations for strategic flexibility and competitive positioning

- Enable rapid response to market opportunities and challenges

- Maintain financial stability and operational continuity through effective capital management

- Support organizational sustainability through optimized resource allocation

Conclusion

Working capital management represents a fundamental aspect of corporate financial management that significantly influences organizational liquidity, profitability, and long-term sustainability. The comprehensive analysis presented demonstrates the multifaceted nature of working capital decisions and their far-reaching implications for business performance and strategic positioning.

Effective working capital management requires a sophisticated understanding of industry dynamics, operational requirements, and financial optimization principles. Future research directions should explore the evolving impact of technological innovations, changing market conditions, and regulatory developments on working capital management practices.

Digital transformation initiatives, supply chain disruptions, and emerging payment systems continue to reshape traditional approaches to working capital optimization, creating opportunities for enhanced efficiency and new challenges for financial managers.

Final recommendations emphasize the critical importance of developing comprehensive working capital management strategies that align with organizational objectives while considering industry-specific requirements and market conditions.

Success in working capital management demands continuous attention, regular performance evaluation, and a willingness to adapt strategies based on changing circumstances and emerging opportunities. Organizations that prioritize working capital optimization position themselves for enhanced financial performance, improved operational efficiency, and sustained competitive advantage in increasingly dynamic business environments.

Related Articles:

- How to Create an Amazon Seller Account: Complete Step-by-Step Guide

- Top 5 Financial Ratios Every College Student Should Know (With Examples)

- How to Register an LLC in America: A Complete Guide for Beginners, Foreigners, and Entrepreneurs

- What is Inbound Marketing: Why Smart American Businesses Are Making the Switch

- Top 5 Best Bookkeeping Software to Work with Accounting: 2025 Guide

- Remote Marketing Jobs: A Step-by-Step Guide to Opportunities and Strategies to Succeed

- What are Accounts Payable? Its Definition, Process, and Best Practices

- 10 Fundamental Accounting Principles Every Business Owner Must Know

- Fixed Index Annuities: Your Way to Financial Confidence and Security

- QuickBooks Excellence: Transform Your Accounting Game with These Powerful Techniques

- Inbound vs. Outbound Marketing: The Great Debate That’s Reshaping Business Strategy

- How to Master Balance Sheet Analysis? Expert Guide with Examples

- Income Statement Formats: Complete 2025 Guide with Examples and Structure

- What Are Current Liabilities And Why They Matter For Financial Success

- Current Assets Essentials: Elevate Your Financial Management Game

- Remote Payroll Jobs: Your Gateway to Flexibility and Financial Growth

- Payroll Advance: Powerful Ways to Enhance Workplace Morale

- Powerful Mobile Marketing Strategies You Must Try

- Best Marketing Tools In An Advertising Plan

- Mastering Revenue Expenditure for Business Success

- Market Research And Its Importance: A Comprehensive Review

- What You Should Know? Notes Payable And Accounts Payable

- Digital Marketing And Strategies: A Comprehensive Review with Examples

- Are Annuities the Best Investment for a Bright Future? A Comprehensive Analysis

- Understanding Capital Expenditure: Definition, Significance, and Its Association in Financial Decision-Making

- Difference Between Accounting And Finance: A Proven Comprehensive Guide For Beginners

- Difference between Annuity due and Ordinary Annuity

- Essential Accounting Software for Small Enterprises

- 5 Best Software For Small Business Accounting

Just started playing and I’m curious about the new mechanics – anyone else notice the glitch in the third level? The vibes are immaculate though.