Mastering Bonus Depreciation for Maximum Savings: Million Dollar Tax Break

Within the intricate environment of business taxation, there is little more substantial relief available to the business as a whole in the short term and strategic benefits from bonus depreciation. This strong tax incentive has helped countless firms to cut their taxes sharply without compromising cash flow and at the same time hastening expansion plans. The knowledge and execution of bonus depreciation plans, with the guidance of professionals, might spell the difference between incurring high tax payments and putting the same money back into the business to fuel its growth.

Bonus depreciation is a deviation of the established approaches of depreciation, permitting companies to expense a large part or, in most situations, the whole cost of qualifying property during the year it is put into service. Qualifying property typically includes tangible assets such as machinery, equipment, and software, but it’s important to consult with a tax professional to determine eligibility. This tax benefit acceleration is an instant value for both small and large businesses, including startups and corporations.

Understanding Bonus Depreciation Fundamentals

Traditional Depreciation vs. Bonus Depreciation

The traditional depreciation works based on the aspect of matching costs with income as time goes by. When a company buys equipment costing $100,000 and has a useful life of ten years, the traditional depreciation method will amortize this expenditure throughout the ten years and thus will deduct around $10,000 per year. Although a methodical approach, this method will postpone the entire tax advantage of the asset purchase.

Bonus depreciation changes this schedule by allowing companies to deduct much more in a given time period. With the existing rules, qualifying assets can be fully expensed under bonus depreciation, such that the full purchase of the equipment of $100,000 could be expensed in the first year instead of over a period of ten years.

The Mechanism of Bonus Depreciation

The bonus depreciation system works under the specific provisions of the Internal Revenue Code, specifically under Section 168 (k). This section changes the normal depreciation schedules, allowing businesses to supplement normal depreciation when they buy qualifying property. This election should be done for the tax year in which the property is put in service.

The step of calculating the computation entails identifying the basis of the asset, verifying that it is eligible for the bonus depreciation, and applying the corresponding percentage rate. The additional amount following the depreciation of the bonus will then undergo the normal ways of depreciation in the recovery period of the asset.

Qualifying Assets and Property Types

Equipment and Machinery

Manufacturing equipment, construction equipment, and technological hardware are the most common examples of bonus depreciation when they fit the requirements. New equipment is usually accorded priority, but recent legislation has extended the list of those eligible to buy some used equipment.

It is determined that the equipment is by system, taking into consideration factors such as the classification of the asset under the Modified Accelerated Cost Recovery System (MACRS), the useful life of the asset, and the condition of acquisition. Equipment with recovery periods of twenty years or less generally qualifies for bonus depreciation treatment.

Software and Technology Assets

Computer software that is either bought or made usually goes into satisfaction of the bonus depreciation, provided it meets the set standards. Off-the-shelf software is considerably simpler to include, whereas the costs of custom software development may need more scrutiny to determine whether to be included.

There are often accelerated depreciation treatments applied to technology infrastructure (servers, networking equipment, and specialized software systems). Yet, it is necessary that businesses document the date of placing in services carefully and that all regulations are followed.

Qualified Improvement Property

Qualified improvement property involves certain kinds of improvements to the existing commercial buildings. Such improvements have to fulfill high standards, such as being installed on interior areas of nonresidential structures and installed after the initial occupants of the building.

They may involve interior renovations, new floor, new lighting system, and a modified layout that will improve functionality. Nonetheless, the types of improvements that are generally not to be treated as bonus depreciation are those associated with enlarging buildings, elevators, or alterations in the structural framework.

Current Regulatory Framework (2025)

Bonus Depreciation Rates and Phase-Out Schedule

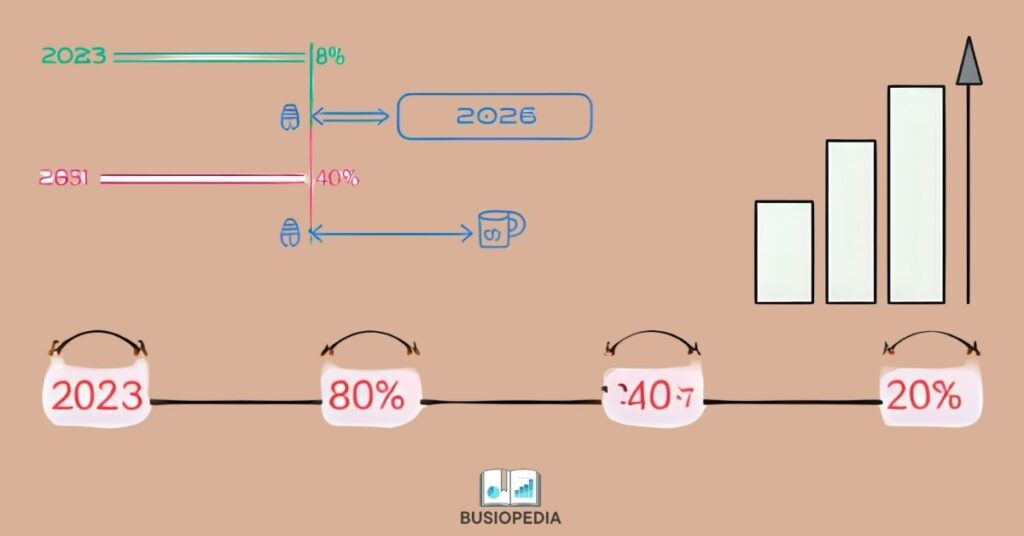

The Tax Cuts and Jobs Act of 2017 codified 100% bonus depreciation against the qualifying property placed in service on or after September 27, 2017, to December 31, 2022. But present policies have a phase-out schedule that lowers these percentages as time goes by.

In 2023, the bonus rate of depreciation was reduced to 80 on property put in service. This rate is steadily dropping by 20 percentage points every year, and in 2024, this rate is 60 percent, and in 2025, this rate is 40 percent. The phase-out remains 20 percent throughout 2026 and finally expires on property placed in service beyond December 31, 2026, unless extending legislation is enacted by Congress.

Special Rules and Exceptions

Some categories of properties are put on long phase-out periods, especially assets with longer production cycles or transportation equipment. These long-term schedules acknowledge the reality of business timing of large capital investments, which makes it difficult to make a proper plan, and also allows more flexibility in planning.

There is also a specific anti-abuse provision adopted by the regulations aimed at avoiding the abuse of bonus depreciation benefits in the form of artificial transactions or arrangements that do not have economic substance. This provision, often referred to as the ‘anti-churning rule’, ensures that the bonus depreciation is not misused for tax avoidance purposes, but rather used for its intended purpose of stimulating business investment.

Strategic Implementation and Planning

Timing Considerations

Bonus depreciation planning has become a sensitive issue that should be considered in terms of time. Year-end planning is key to maximizing benefits, as the year-end placed-in-service date can dictate eligibility and rates to be charged. The bonus depreciation rates are likely to be higher before moving to lower rates in the future, and this often causes businesses to speed up the delivery of equipment and installations to get the bonus rate.

Nonetheless, timing strategies have to balance the tax advantages with the operational requirements and the cash flows. It is hardly cost-effective to buy equipment whose real purpose is to get a tax deduction and not an actual business need that can draw audit attention.

Cash Flow Optimization

Bonus depreciation generates short-term cash flows by decreasing the amounts on current-year taxes. The benefits of these savings can be used to finance more investments, minimize the level of borrowing, or cushion funds in case of uncertainty in the economy. Most businesses reinvest the bonus depreciation tax savings in additional qualifying asset purchases, which has a compound effect.

The cash flow effect is not limited to federal taxes, where most states follow the federal bonus depreciation regulations, increasing the benefits. Nonetheless, certain states no longer align with federal provisions, so special scrutiny must be given to the federal and state tax implications.

Integration with Overall Tax Strategy

Bonus depreciation is most effective when incorporated with overall tax planning concepts. This includes planning in line with the Section 179 expensing election, planning around Alternative Minimum Tax implications, and multi-year tax planning situations.

Accelerated depreciation also presents business implications in terms of taxes in the future. Although bonus depreciation has short-term gains, it decreases depreciation deductions in the future, which can raise taxable income in the future. This time change needs the need to evaluate the calculated tax rates and business conditions.

Limitations and Considerations

Income and Business Limitations

Bonus depreciation benefits come with a range of limitations that may impact their usefulness. Additional deductions may not be of direct assistance to businesses that have net operating losses, but they may be able to offset future income or be carried back to prior years in some situations.

The rules of the passive activity may also restrict the bonus depreciation benefits of particular investors and business formations. Such intricate rules need to be analyzed closely to make sure that deductions are giving any practical tax benefits and not suspended indefinitely.

Alternative Minimum Tax Implications

Although the Tax Cuts and Jobs Act repealed the corporate Alternative Minimum Tax (AMT), AMT computations can still apply to individual taxpayers and also to some business entities that are subject to it, and presents benefits to bonus depreciation. The AMT system has various depreciation regulations that may limit or cut down the advantage of rapid depreciation procedures.

This implies that the implications of AMT need advanced examination of tax planning and professional advice in order to optimize the overall tax approaches and take into account possibilities of regular taxation and AMT.

Practical Examples and Case Studies

Manufacturing Business Sample

Take an example of a manufacturing company that buys new production equipment in 2025 to the tune of $500,000. The initial deduction under the traditional depreciation would be about $71,430 in the first year under MACRS, which is done using seven years. Nevertheless, given a 40 percent bonus depreciation in 2025, the firm can write off $200,000 upfront and regular depreciation on the remainder of the basis, which is $300,000.

This expedited deduction offers direct tax savings of about $42 000 to $50 000 (subject to tax rates), which is a tremendous enhancement of cash flow and can be used to fund further investments or operations.

Technology Company Scenario

A technology services company that invests in servers and network equipment to the tune of 200,000 dollars would want to maximize its tax benefits, using bonus depreciation. This is because with the qualifying equipment, the bonus depreciation overshadows the possibility of the firm deducting the full purchase price in the year of installation, thus enabling significant tax savings that could be used to finance software development or market expansion activities.

Professional Guidance and Implementation

The Importance of Expert Consultation

Due to the sophistication of the bonus depreciation rules and their interplay with other tax applications, a professional is needed to maximize the exercise. Tax professionals are able to examine particular situations, distinguish qualifying assets, and formulate strategies, which can benefit to the highest level within compliance.

Professional consultation cost is often a small investment in comparison to the tax savings that might be achieved with proper bonus depreciation planning and execution.

Documentation and Compliance Requirements

Implementing the bonus depreciation successfully demands careful documentation of asset purchases, dates when they are placed in service, and percentages of business use. Keeping good records safeguards businesses in case they are subjected to an audit and enables benefits that are claimed to be justifiable.

Key Takeaways

To realize bonus depreciation, it is important to understand some of the fundamental principles that, in business taxes, may play a significant role:

Short-Term Financial Effect: Bonus depreciation is associated with a massive immediate tax deduction, and 2025 allows a 40 percent immediate deduction of qualified assets. This will translate into meaningful improvements in cash flows that can finance operations, decrease the amount of borrowing required, or quicken growth efforts.

Time is of the essence: The phase-out plan creates timing as a necessity. As rates fall to 40 percent in 2025 to 20 percent in 2026 and then fully expire, companies need to play the game of buying assets to maximize benefits.

Asset Qualification Matters: Not every business purchase is eligible for bonus depreciation. Being aware of the difference between a qualifying and non-qualifying equipment, software, and improvements versus non-compliant assets prevents the loss of opportunities and compliance challenges.

Compatibility with Tax Strategy: Bonus depreciation is most effectively used in coordination with other tax features, such as Section 179 expensing, standard depreciation periods, and business tax planning goals.

Documentation Requirements: Adequate documentation and record-keeping relating to asset placement dates and business use percentages, as well as qualification criteria, are necessary to prove claimed benefits in the event of an audit.

Professional Guidance Value: Most businesses should consider professional consultation a valuable investment because bonus depreciation regulations are complex and interact with other tax regulations.

Conclusion

Bonus depreciation is one of the most beneficial tax planning tools for a business that conducts qualifying asset investments. Although the present-day phase-out plan generates an element of urgency to maximize gains, the strategic benefits of faster depreciation go well beyond the short-term tax savings.

By comprehending the qualification criteria, time factor, and strategic implications of bonus depreciation, businesses can make informed choices that can maximize tax advantages as well as business outcomes. With the ongoing changes in the regulatory framework, business tax planning that considers the prospects of bonus depreciation is important to stay abreast of the changes.

Bonus depreciation is a one-million-dollar potential that is not only beneficial in terms of the immediate tax savings offered, but also in terms of strategic flexibility and growth capabilities offered by the savings. When businesses are willing to spend on their future, bonus depreciation provides an effective tool to retain more capital to work productively in the company instead of exhausting it on taxes.

With the skill of bonus depreciation and its combination with complete business planning, companies can convert substantial tax liability into competitive advantages, growth financing, innovation, and long-term success in the form of smart tax planning and strategic asset management.

Related Articles:

- What is Working Capital and How to Calculate: Your Complete Guide to Financial Success

- How to Create an Amazon Seller Account: Complete Step-by-Step Guide

- Top 5 Financial Ratios Every College Student Should Know (With Examples)

- How to Register an LLC in America: A Complete Guide for Beginners, Foreigners, and Entrepreneurs

- What is Inbound Marketing: Why Smart American Businesses Are Making the Switch

- Top 5 Best Bookkeeping Software to Work with Accounting: 2025 Guide

- Remote Marketing Jobs: A Step-by-Step Guide to Opportunities and Strategies to Succeed

- What are Accounts Payable? Its Definition, Process, and Best Practices

- 10 Fundamental Accounting Principles Every Business Owner Must Know

- Fixed Index Annuities: Your Way to Financial Confidence and Security

- QuickBooks Excellence: Transform Your Accounting Game with These Powerful Techniques

- Inbound vs. Outbound Marketing: The Great Debate That’s Reshaping Business Strategy

- How to Master Balance Sheet Analysis? Expert Guide with Examples

- Income Statement Formats: Complete 2025 Guide with Examples and Structure

- What Are Current Liabilities And Why They Matter For Financial Success

- Current Assets Essentials: Elevate Your Financial Management Game

- Remote Payroll Jobs: Your Gateway to Flexibility and Financial Growth

- Payroll Advance: Powerful Ways to Enhance Workplace Morale

- Powerful Mobile Marketing Strategies You Must Try

- Best Marketing Tools In An Advertising Plan

- Mastering Revenue Expenditure for Business Success

- Market Research And Its Importance: A Comprehensive Review

- What You Should Know? Notes Payable And Accounts Payable

- Digital Marketing And Strategies: A Comprehensive Review with Examples

- Are Annuities the Best Investment for a Bright Future? A Comprehensive Analysis

- Understanding Capital Expenditure: Definition, Significance, and Its Association in Financial Decision-Making

- Difference Between Accounting And Finance: A Proven Comprehensive Guide For Beginners

- Difference between Annuity due and Ordinary Annuity

- Essential Accounting Software for Small Enterprises

- 5 Best Software For Small Business Accounting