Understanding Capital Expenditure: Definition, Significance, and Its Association in Financial Decision-Making

Capital expenditure, usually known as CapEx, is a main factor of financial planning. It normally depicts the investments in the long-term assets (property, plant, and equipment) that are assumed to give value for more than one accounting period. Investment in capital expenditures is most important in order to get expansion in business, business’s operational efficiency, technological development to meet competition available in the market.

The capital expenditures are long-term in nature and recorded in the balance sheet as incurred. They are incurred to acquire any asset of the business, so these are depreciated over the useful life of the asset. Understanding the behavior and utilization of capital expenditure is most important for all stakeholders, including all tiers of management, investors, and financial analysts, as these directly affect cash flow, profitability, liquidity, and valuation of the business.

Definition and Essence of Capital Expenditure

Capital expenditure encompasses any outlay of capital by a business to acquire or develop tangible assets. For example, purchases of machinery, construction of buildings in order to get benefits from them for more than one fiscal year, developing IT infrastructure to meet technological challenges, and acquiring vehicles.

Intangible assets, like patents and software, may also be considered Capital expenditures if they are expected to provide long-term economic benefits.

The main characteristic that differentiates capital expenditures from revenue or operational expenditures is their long-lasting nature. Capital expenditures are recorded as assets on the balance sheet under the heading of long-term assets, so they are not consumed within the current accounting period.

Eventually, these assets are consummately reduced in their value through depreciation (for tangible assets) and amortization (for intangible assets).

According to the International Financial Reporting Standards (IFRS) and Generally Accepted Accounting Principles (GAAP), a cost is entitled as capital expenditure if it is incurred to:

- Acquire a new asset in the business.

- Increase the capacity and efficiency of an available asset.

- Also, extend the useful life of an asset for future benefits.

- Strengthen the quality of output or services rendered by the asset.

Significance of Capital Expenditure

Capital expenditure plays a vital role in shaping an organization’s long-term path. Its importance is multi-faceted with respect to financing and investing.

Strategic Expansion: Capita Expenditure offers companies to build new facilities, access new markets, and bring in new products. It is normally connected with long-term strategic objectives of the business.

Technological Upgrades: Acquiring innovative equipment and advanced technology increases productivity, quality of products and services, and cost-effectiveness, which helps companies remain competitive in their respective industries.

Value Creation: Proper capital investment in asset acquiring increases potential earnings, which leads to improved shareholder value as well as the reputation of the business.

Signal to Investors: Capital investment signals the investors about management’s faith in the future potential of the business, hence touching investor sentiments and stock prices.

Tax Planning: Capital Expenditure results in depreciation, which is a non-cash expense, minimizing taxable income, giving tax benefits in the long-term scenario.

Planning and Budgeting for Capital Expenditure

Capital budgeting must be carefully planned because it directly affects the financial condition and cash flow of the company. Usually, capital budgeting consists of the following stages:

Investment Opportunities Identification: Managers cover areas to be extended, replaced, or adjusted.

Project Evaluation: Various methods are used to determine the profitability of projects. They are:

Net Present Value (NPV): Calculates the present value of all expected future cash flows from the cost of the investment.

Formula of NPV:

Where:

Ct = Cash inflows at time t

r = Discount Rate

t = Time Period

C0 = Initial Investment

Internal Rate of Return (IRR): Rate of discount at which NPV of all future cash flows becomes zero.

Formula for IRR:

Where

Ct = Net cash inflows during the period t

C0 = Total initial investment

IRR = Internal rate of return

t = The number of time periods

Payback Period: It is the period of time (in months or years) to recover an initial investment.

Formula for Payback period: (For even cash flows)

Formula for Payback period: (For uneven cash flows)

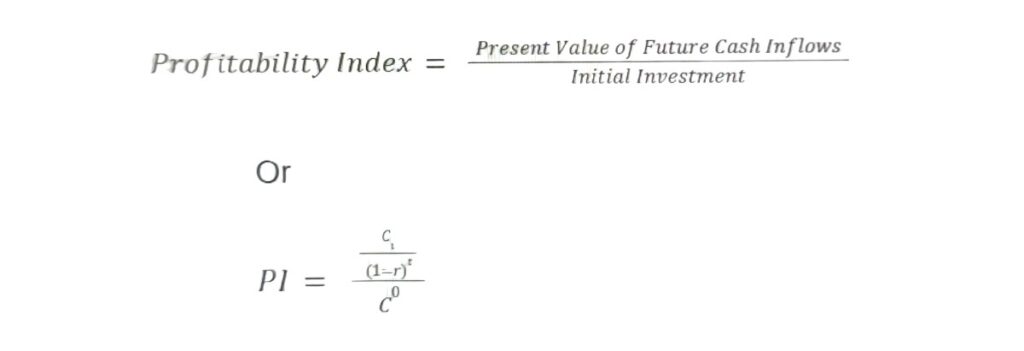

Profitability Index (PI): It is used to evaluate the relative profitability of an investment. It tells us how much value is created for each dollar invested.

Formula for PI:

Capital Rationing: It is a financial strategy in which a company binds itself to invest in new projects, although they are profitable, due to scarce resources or strategic priorities.

Approval and Implementation: When projects are selected, they need to be approved and implemented within the permitted budget.

Post-Implementation Review: Performance is measured against intended results in order to measure the effectiveness of the business.

Accounting Treatment and Reporting of Capital Expenditure

Capital expenditures are recorded as assets in the balance sheet under the heading of Non-current assets. The cost of an asset is distributed over the useful life of the asset for the calculation of depreciation or amortization.

For example, suppose a firm obtains $100,000 worth of equipment with 10 10-year useful life with no salvage value. In that case, we assume the straight-line method to calculate depreciation expense so that it will charge $10,000 as depreciation expense every year.

The impact of Capital Expenditure is reflected in:

Balance Sheet: Increase in non-current assets.

Cash Flow Statement: Under investing activities, as a cash outflow.

Income Statement: Indirect effect by way of depreciation expense.

Transparency of Capital Expenditure reporting is extremely crucial to analysts and investors. Plans for capital spending are typically disclosed by companies within their investor presentations and financial reports.

Capital Expenditure Challenges

Capital expenditure decisions play a crucial role in the life of a business, but they also face some challenges from market behaviours.

High Uncertainty: It is very difficult to anticipate long-term returns with market volatility, technological innovations, and economic conditions of the business world, as well as the country in which the business exists.

Capital Intensity: Business sectors such as manufacturing or energy are capital intensive, and they require a large amount of capital to produce goods and services, and their high Capital Expenditure can be liquidity-straining.

Financing Challenges: projects of capital expenditure are big, and they need debt or equity to accomplish. They also affect the firm’s cost of capital and capital structure.

Conclusion

Capital expenditure is more than a numbers game; it is a strategic long-term investment to acquire non-current assets for the business. Strong planning of capital expenditure helps in achieving long-term objectives, technological innovation, and enhancing value creation. But the complexity and potential risks involved in capital budgeting require extreme scrutiny and careful management.

On the other hand, all stakeholders must appreciate and support the capital expenditure decisions made by the concerned department in order to understand financial statements, evaluate business performance, and help make good investment decisions.

Related Topics: