Difference between Annuity due and Ordinary Annuity

There are two types of annuities in financial structure: an annuity due and ordinary annuity. These annuities consist of a series of equal payments that are made over time, but they both have differences in the timing of these payments.

All payments are made at the end of each period in an ordinary annuity, like bond coupon payments; in annuity due, payments are made at the beginning of each period, like rent or lease payments.

The main difference exists in an annuity due and ordinary annuity is the difference in the timing of payments that affects the present and future value of these annuities. Understanding the main difference between annuity due and ordinary annuity concepts is important for making good financial decisions with respect to investment, loans, and retirement planning.

What is the Annuity Due?

Annuity due is a series of equal payments that is made at the beginning of each period over a fixed duration (e.g. for 50, 60 or 100 years).

Main characteristics of annuity due:

Payment interval:-

Payments are made at the beginning of each period (e.g payments of rent are paid at the beginning of each month, insurance payments are also paid at the start of each month).

Fixed Amount:-

Payments that are paid for an annuity due have a fixed amount of money for all periods (e.g. if you make the first payment of an annuity due is $100, then you will make all remaining payments of the same amount of $100 for the remaining period of the contract).

Fixed duration for making payment:-

In annuity due, payments are made within the same interval of time( most likely 12-month duration to pay each payment of the annuity at the start of the period).

Impact of interest rate:-

As we studied, the payments are made at the start of each period in an annuity due. Hence, the present value is higher than compared of an ordinary annuity ( where payments are made at the end of each period).

Case:-

You pay $1000 rent at the beginning of each month for 12 months.

Key details:-

Total amount = $1000

Number of payments = 12

Payment interval = at the beginning of each month

Payment Schedule:-

At the start of 1st month = $1000

At the start of 2nd month = $1000

And so on

At the start of the 12th month = $1000

The future value of the annuity due is higher than ordinary annuity because an annuity due has more compounding periods than an ordinary annuity.

Uses of Annuity Due:-

Rent payments. Tenants normally pay rent payments at the start of each period (a period normally contains one rent payment, but it can also be paid quarterly or annually as per the contract).

Lease agreement

Some individuals or businesses make a lease agreement for equipment, land, and other property, so the payments of lease payments are made at the beginning of each period.

Insurance premium

Most individuals make a contract with insurance companies for the protection of their assets, so insurance companies require advance payments for every period of that contract of insurance.

Tuition fee

Some educational institutions require tuition fees at the start of each semester.

The annuity due is the series of payments made at the beginning of each period. Following is the formula to calculate the annuity due:-

The formula for the present value of an annuity due is:

Where:

PV = Present Value

P = Payment amount per period

i = Interest rate per period

n = Number of periods

The formula for the future value of an annuity due is:

Where:

FV = Future Value

P = Payment amount per period

i = Interest rate per period

n = Number of periods

Understanding Ordinary Annuities with Examples: A Beginner’s Guide

Finance can appear terrifying to beginners, but it plays a crucial role in everyday life. Whether you are investing in long-term plans, paying off student loans for your studies or preparing for retirement in order to get a bright future, knowing some basic financial concepts will assist you in making wiser choices. Finance has many concepts to understand its importance, and ordinary annuity is one of the most important concepts. This study for beginners breaks down what an ordinary annuity is, how it works, and why it is important, especially for students just starting their financial journey from scratch and who want to become role models in the world of finance.

What is an Ordinary Annuity?

An ordinary annuity is a chain of equal payments made at the end of every period. These payments are made at regular intervals over a stipulated period. This aspect of “timing” is what makes annuity “ordinary.”

Major Features of Ordinary Annuity:

Equal Payments: In an ordinary annuity, every payment in the series is of an equal amount.

Fixed Intervals: Annuity Payments are paid at fixed intervals (monthly, quarterly, annually, etc.) according to the annuity contract basis.

End of Period: Annuity Payments are paid at the end of every interval.

For example, if you deposit $500 into a savings account at the end of each month for ten years, you are creating an ordinary annuity.

Difference between Ordinary Annuity and Annuity Due

It is important to make a difference between an ordinary annuity and an annuity due. These both involve a series of payments, but the main difference is the timing of the payments. In an ordinary annuity, the payments are made at the end of the period, and in an annuity due, the payments are made at the beginning of the period.

Repayments of loans (like student loans or mortgages) are ordinary annuities, while payments of rent or insurance premiums are annuities due.

Examples of Ordinary Annuities

Here are a few real-life examples for a better understanding of ordinary annuities.

Loan Payments: When you make a payment on a loan or mortgage, you usually pay a fixed amount at the end of each month.

Savings Plans: Depositing a fixed amount of payment into a savings account at the end of each period is an example of investing through an ordinary annuity.

Pension Plans: Receiving fixed retirement payments every month after retiring also follows the rules of ordinary annuities.

How Does Ordinary Annuity Work?

When you make or receive regular payments at the end of each period, two main financial facets come into play:

Present Value (PV): It is the value of future payments that you make as an ordinary annuity in today’s dollar value.

Let us examine the present value of ordinary annuity concept clearly for a better understanding:

Present Value of an Ordinary Annuity

The present value of an ordinary annuity comes into play when you wish to know how much a sequence of future payments is presently worth. For instance, if you are to receive $5,000 every year for 10 years, the present value shows you how much such payments are worth in present money today.

Where:

PVA = present value of an annuity

P = Payment amount per period

i = Interest rate per period

n = Number of periods

Future Value (FV):

It is the value of today’s dollar at some future date, considering some interest or investment growth.

Let us examine the future value of ordinary annuity concept clearly for a better understanding:

Future Value of an Ordinary Annuity

The future value of an Ordinary Annuity assists you in calculating how much your chain of payments will be worth in the future, particularly applicable in savings and investment planning programs.

Where

FVA = Future value of an ordinary annuity

P = payment amount per period

i = interest rate per period

n = Number of periods

Awareness of these formulas can assist you in determining investment options and loan terms.

Why is it most Important to know About Ordinary Annuities in order to make your plans?

As a learner, you might not be thinking about retirement or huge investments yet. Howbeit, understanding ordinary annuities guides with:

Budgeting: Budgeting supports you in managing your regular expenses like repayments of loans, mortgages or subscriptions.

Savings Goals: Saving is the most important factor in every life. Planning helps you to identify your future needs with the best saving plans, which give you the option of a bright future.

Financial Literacy: Literacy is all about the awareness of financial resources in order to make better decisions for financial careers. Awareness of every financial facet assists you in analysing economic conditions that may provide an opportunity for your financial growth.

Common Misconceptions

- An ordinary annuity is only for retirement.

- Annuities are not limited to just retirement programs, but annuities in general may pertain to many situations involving regular payments for both saving and borrowing plans.

- Interest does not affect annuities.

- Indeed, a little change in interest rate can affect the present or future value of an annuity over time.

- Annuities are sophisticated.

- Annuities are not as complicated as they appear. Once you understand the core concept of annuities (equal payments over some time), the rest is just putting the value in formulas and understanding the time value of money.

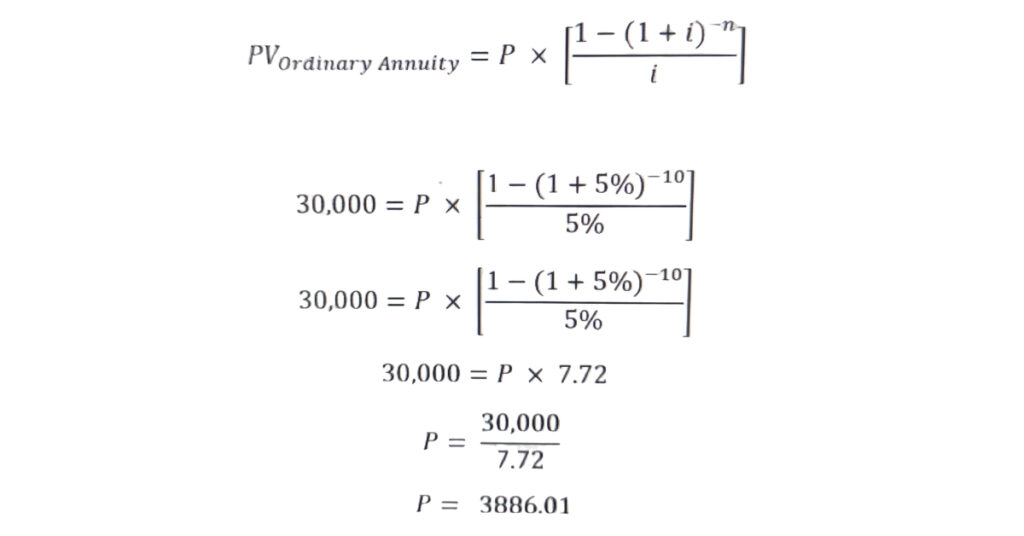

Student Loan Example

Let us say you have a student loan of $30,000 with an annual interest rate of 5% to be repaid over 10 years. Applying the ordinary annuity formula, you can estimate your monthly payment and total interest to be paid over the life of the loan.

The amount of the monthly payment would be $3,886 approximately, and the total interest to be paid would be $8,860

Where:

PV = present value of an annuity

P = Payment amount per period

i = Interest rate per period

n = Number of periods

Read more: Accounting Software for Small Enterprises

Conclusion: Annuity Due And Ordinary Annuity

To sum up the topic of annuity due and ordinary annuity, it pertains to equal payments made at the beginning, and end of each period respectively. For saving, investing or repaying a loan, understanding how these payments work and how to calculate their value, can provide you with huge control over your financial future.

Here are the things that you should remember:

- Ordinary annuities are everywhere, in loans, mortgages, savings, and retirement plans, and annuity due rent, lease, and insurance premium.

- The main key is the “timing of payments (end of period).”

- Awarding the present and future value of annuities assists you with better planning decisions.

- Financial literacy grows with understanding such core but powerful concepts.